Pan De Vera, a fellow member of

UITF FB group, has started blogging which inspired me to update this blog,

His latest post (

see here) is about his thoughts on peso cost averaging (PCA) as related to investing in UITFs.

There is much discussion, pros and cons, in our FB group. And sometimes it can get acrimonious. But there is not enough space on FB to really explain your side of the issue.

So here's my take on the subject. This is the story of Hal.

Hal, in the evening of December 31, 2013, decided that as part of his New Year resolution he will start saving 1,000 pesos per month. He had already built up an emergency fund. This time it will be for investment. He was looking forward to starting his own family in 5 years.

He heard about the Unit Investment Trust Fund (UITF) from a teller of BPI. His employer credits his salary every 15th and 30th of the month to this bank.

Thankfully, the teller did not induce him to get a

VUL. 😉 So UITF it was.

He chose the BPI Philippine Equity Index Fund and opted for a Regular Subscription Plan (RSP). The bank would credit his fund account every 15th of the month; or the next banking day, if the 15th is a weekend or a holiday.

On New Year's eve of 2017, he thought that it was a fine time to settle down by February 2018.

So he redeemed on January 29, 2018. Here's how much he got.

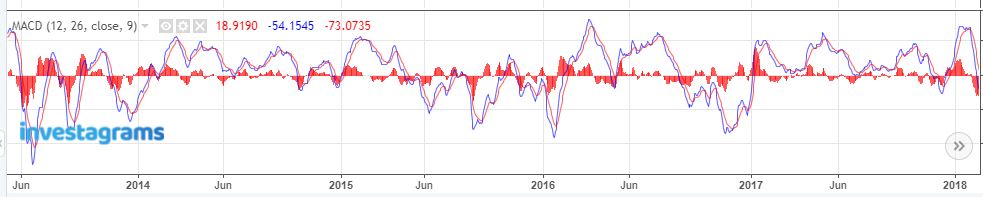

"What if I followed the MACD buy signals?" he thought.

Here's the MACD for the period courtesy of Investagrams.

Click on the

MACDBuy tab on the worksheet above to find out what Hal learned.

What if Hal followed the buy and sell signals of the MACD? Well, he would not sell, either to take profit or to cut losses, because he is a straight PCA guy like many in our FB group.💓

But it was good that he did not buy and sell. He would have lost some of his capital. I can show here the worksheet but I'd rather that you do your own backtesting, a favorite mantra of the

ZFT crowd, of the data.

Hal would have done better if he used what I call the Strategic Peso Averaging Method (SPAM). That will be a subject of my next post.

BTW, try changing the monthly amount on the straight PCA sheet.